Valuing a pre-revenue startup/company can be a difficult process. It differs from a mature business valuation, in which founders review the company's accounting reports to assess its value and prospects. In this case, the company obviously lacks these records, so you'll have to adopt other non-traditional startup valuation methods.

What is pre-revenue?

Breaking the word "pre-revenue" down, you can find that it comprises two words, "pre" and "revenue." As you may know, "pre" means before, while "revenue" refers to the money a business makes from selling its products and services.

In other words, when you say that a business is at the pre-revenue stage, it is not yet generating funds. As such, the term refers to startups with concrete business plans, prototypes, and products that haven't generated revenue from customers.

What is pre-revenue valuation?

Pre-revenue valuation measures a startup's worth, and it's an important activity for investors and the business owner. From an owner's standpoint, they can get an idea of how much money they can raise. From the investor's standpoint, they'll need to know how much equity they stand to get and whether the company has good potential for growth and return on equity.

Investors often get equity ownership in return when they invest in startups. They, therefore, measure the worth of the equity they own and what they stand to gain by valuing the company. Usually, the goal is a higher valuation.

As a founder, on the other hand, you want to give an accurate valuation of your firm so that you don't give investors high hopes. Although an inflated evaluation may fetch you more pre-revenue startup funding, it may give a bad impression of your business to existing and prospective investors if you fail to deliver.

How to value pre-revenue startup

Valuing a startup is not as easy as with an established or growing company. Valuation requires a company's financial forecast, statements, and quantitative analysis, but in the case of a pre-revenue firm, there is no such data.

This means that traditional valuation methods may not be appropriate for a startup. Pre-revenue startup valuation is usually tricky, requiring thorough knowledge and experience.

Before valuing a pre-revenue startup, there are many things to consider, including the management team, market trends, the marketing risks involved, and the demand for the product. Below are the non-traditional methods used for pre-revenue startup valuation;

- Berkus Method

The Berkus method is a simple valuation method that uses estimation. It was developed by an angel investor named Dave Berkus and values a business based on its value drivers. These drivers include the business idea, prototype, strategic relationships, management team, technology, and rolled-out products.

The Berkus method works with the assumption that the startup will generate $20 million in revenue by the fifth year. The investor goes further to check the possibility of the company making this sum by allocating an amount of up to $500,000 to the different lines or value drivers in the organization.

The idea is usually that each value driver increases the chance that the company will meet its goals. Normally, the value of each driver does not exceed $5000.

So, for example, the estimation can be;

- Business Idea – $500,000

- Strategic Relationships – $500,000

- Management Team – $500,000,

- Rolled Out product – $500,000

- Technology – $500,000.

From this estimation, the total startup valuation is $2.5 million. Usually, the Berkus method expects a startup valuation of $20 million in the 5th year of business. So, when you've gotten the estimated valuation, you then assess the possibility of these value drivers increasing the business's value up to $20 million or more in the next five years.

- Scorecard Method

The Scorecard valuation method, also known as the Benchmark method, was developed by Bill Payne. This method derives a company's valuation by comparing the business venture to other firms within the business sector or region.

Typically, it's like saying that if a company is similar to another, valued at $2.5 million, then the company's value should be $2.5 million.

However, the Scorecard method works with a benchmark and so compares values based on some vital factors, including;

- The size of the business opportunity

- The strength of the management team

- The product or technology at the center of the business

- The competitive environment of the business

- The existing marketing or sales channels

- The need for capital

- Other investment-specific information

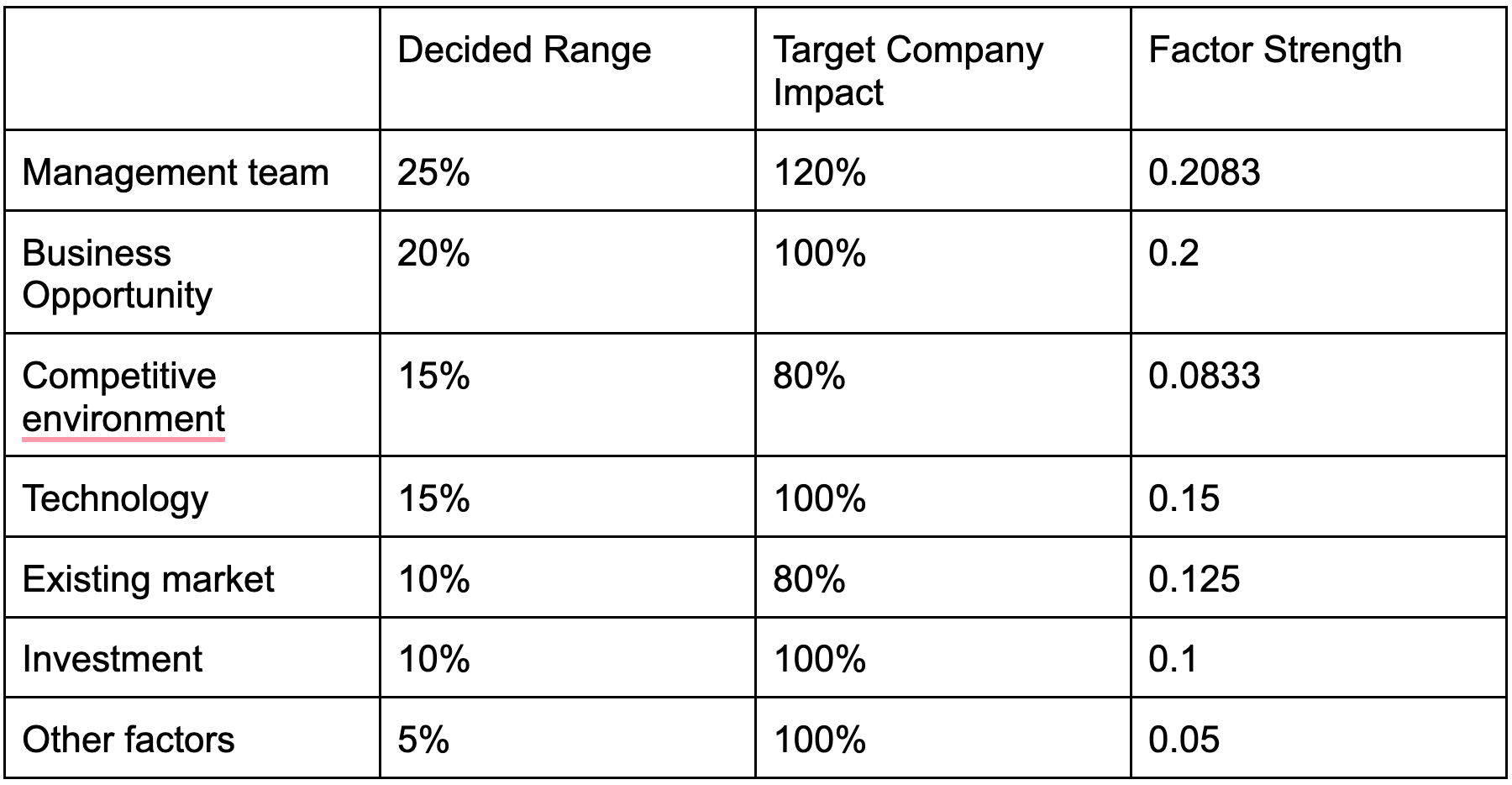

Each of these evaluation parameters is assigned a weight. For example, the pre-percentage weighting for the success factors can be:

- Management Team – 25%. The quality of your founding team plays a critical role in your business's success. Bill Payne asserts that "In building a business, the quality of the team is paramount to success. A great team will fix early product flaws, but the reverse is not true."

Assume that Elon Musk is a shareholder in the company. Your startup stands a better chance for a high return.

- Business Opportunity – 20%. Business opportunity to the size of your market (people interested in your products). The bigger your potential market, the better.

- Competitive environment – 15%. The market is highly competitive, and as a new company, that is already a risk.

- Technology – 15%.

- Existing market – 10%.

- Investment – 10%

- Other Factors – 5%

The next step in this valuation process is to assign a target company impact (in percentage form) to each parameter and calculate the factor strength by dividing each parameter by the matching target company impact.

Lastly, multiply the valuation benchmark value by the sum of the factor strength. Using the valuation of an abstract company ABC, the valuation benchmark value is $2.5 million. The sum of the factor strengths is 0.9166.

2.5 × 0.9166 = $2.915 million

- Chicago Method

The Chicago First method is another valuation method by venture capital and private equity firms for valuing early-stage companies. This method is based on predicted cash flows, combining the market and the company's fundamental analysis.

To achieve its goal, it creates different cases: the best-case, mid-case, and worst-case scenarios for the firm and sets financial forecasts for each. A best-case scenario is based on company performance, assuming that all things go as planned, while the worst-case scenario is the opposite.

The idea is to project the cash flow of the company in the three scenarios to make informed decisions.

Assuming company ABC is to invest $1,000,000 in a pre-revenue startup, here is how the three scenarios play out. The best-case scenario projects a financial performance where investors have a 50% likelihood of a high profit margin.

In the mid-case scenario, where investors have a 30% chance of profits, and in the worst-case scenario, where investors have a 20% chance and lose their investment to get a weighted sum average, all of the probabilities are put together.

- Venture Capital Method

Developed in 1987 by Harvard Business School Professor Bill Shalman, the pre-revenue venture capital method combines components of a multiples-based and discounted cash flow (DCF) valuation approach.

To determine pre-money valuation, it first works out post-money valuation using industry metrics. As such, it uses five forecasted years of revenue, then awards trading multiple net profits based on the industry standards, and lastly, subtracts the anticipated return on investment.

The venture capital method is broken down into two steps, which are:

- Calculate the terminal value of the business, and

- Track expected ROI and investment amount.

Where ROI = terminal value / post-money valuation, and Post-money valuation = terminal value / anticipated ROI.

Terminal value is the expected selling price of a startup in the future (likely the next 5-8 years as the average for early-stage equity). To work out anticipated ROI, understand that the industry standard for early-stage investment requires all investments to demonstrate the possibility of a 10-40x return.

Terminal Value = projected revenue profit margin P/E (stock price-to-earnings ratio). A P/E ratio of 5 means the stock is valued at 5 x $1 in earnings.

For example, a Saas company projects $10 million in 5 years, a profit margin of 10%, and a P/E ratio is 20, and the investor wants an ROI of 10x on $1 million.

First, calculate the terminal value.

Terminal value = $10 million*10%*20 = $20 million.

Second, calculate pre-revenue valuation. Pre-Money Valuation = Terminal value / ROI – Investment amount

Pre-revenue valuation = $20 million/10 – $1 million = $1 million.

- Risk Factor Summation method

The risk factor summation considers a lot of factors in determining the pre-money valuation of pre-revenue companies. It exposes investors to a myriad of risks that a venture must put in check to arrive at a lucrative exit. Typically, it analyses twelve types of risks, including;

- Management,

- Stage of the business,

- Legislation/political risk,

- Manufacturing risk,

- Sales and marketing risk,

- Funding/capital raising risk,

- Competition risk,

- Technology risk,

- Litigation risk,

- International risk,

- Reputation risk, and

- Potential lucrative exit.

Each of these risks is assessed as follows:

+2 - very positive

+1- positive

0 - neutral

-1 - negative

-2 - very negative

After analyzing the risks, it goes further to assign a monetary value to each risk, adding or subtracting based on the risk rationale. So,

- -2 (very negative) = subtract $500,000

- -1 (negative) = subtract 250,000

- 0 (neutral) = add/subtract nothing

- +1 (positive) = add $250,000

- +2 (very positive) = add $500,000.

This means that the pre-revenue startup valuation will increase by $500,000 for every +2 and by $250,000 for every +1. On the flip side, pre-revenue startup valuation will reduce by $500,000 for every -2 and by $250,000 for every -1,

For example, company XYZ has no reputation risk (+$500,000), manufacturing risk (+$500,000), litigation risk (+$500,000), and marketing risk (+$500,000) but has high management (-$500,000) and low competition risk (+$250,000). The pre-money valuation would be $1.75M.

To get a holistic view of a startup's pre-revenue value, it's best to combine this method with the scorecard method.

- Book Value Method

The book value or asset-based valuation method is one of the simplest pre-revenue valuation methods, as it assesses the real value of the startup. The book value of a pre-revenue startup is derived by subtracting the company's total liabilities from the total assets.

So, let's assume that the total asset of a startup is $6 million and the total liabilities is $2.5 million. The pre-revenue startup book value = $6 million-$2.5 million= $3.5 million.

The limitation of this method, however, is that it looks at the startup from its present state rather than making future forecasts. Investors are more concerned about the future of a startup, and the book value method doesn't take that into account.

- Cost-to-Duplicate Method

The cost-to-duplicate method evaluates the cost of duplicating the startup elsewhere to determine the pre-revenue startup value. However, it doesn't include the value of intangible assets. In other words, you calculate the value of the startup's physical assets (based on the market value) and sum them up.

Include charges for research & development, patents, and product prototypes. Similar to the book value method, this method does not examine a company's future potential.

- Comparable Transactions Method

The comparable transactions method is based on precedent, that is, similar businesses. So, you're trying to answer the question, "How much did it cost to acquire startups like mine?"

To get the valuation, therefore, you find revenue multiples for similar companies in the industry. For example, a fictional tech startup company, Rapidaccount, produces 5x to 7x the prior year's net sales. Since your company lacks a robust infrastructure and production capacity compared to Rapidaccount, you could use a lower multiplier (5x or lower) to assess your company's value.

Bottom Line

Every startup founder needs a valuation to have a better shot at raising capital. Investors also consider valuation an important due diligence procedure to go ahead with pre-revenue funding. However, in valuing a pre-revenue startup, there are three basics to note.

First, pre-venue startup valuation is a difficult process because there is no data to draw insight from. Secondly, there are no precise valuations for early-stage companies.

And finally, there is no one-size-fits-all method for valuing a pre-revenue company. You can combine two methods for a holistic valuation. In the end, even with the most effective pre-revenue valuation formula, the outcome is still just an estimate.